1. Introduction

I’ll never forget opening my first Health Savings Account (HSA): it felt like unlocking a secret vault of tax savings and investment power. Today, I want to walk you through how to optimize your Health Savings Account (HSA) contributions, ensuring every dollar works harder for you—both now and in retirement. Whether you’re brand new to HSAs or looking to refine an existing strategy, this guide provides actionable, step-by-step advice.

By the end of this deep dive, you’ll know:

What makes HSAs unique and why they deserve a spot in your financial plan

How to stay within IRS rules and avoid penalties

Smart tactics to automate and adjust your contributions

Ways to integrate HSA funding into your monthly budget

Investment strategies to maximize long-term growth

Let’s get started.

2. Understanding HSAs and Their Benefits

2.1 What Is an HSA?

A Health Savings Account is a tax-advantaged account you pair with a High-Deductible Health Plan (HDHP). Unlike a Flexible Spending Account or a Health Reimbursement Arrangement, the money you contribute to an HSA is yours forever—no “use-it-or-lose-it.” You decide when and how to spend it on qualified medical expenses, from prescriptions and doctor visits to dental and vision care.

Key attributes:

Portability: You own the account—even if you change jobs or health plans

Rollover: Unspent balances carry forward indefinitely

Flexibility: Use it now for medical costs or let it grow tax-free and tap it later

2.2 Key Tax Advantages

The true power of HSAs lies in their triple tax benefit:

Pre-Tax Contributions lower your taxable income immediately

Tax-Free Growth means interest, dividends, and capital gains aren’t taxed as long as funds remain invested

Tax-Free Withdrawals for qualified medical expenses ensure you never pay tax on distributions

This unique structure makes HSAs one of the most efficient savings vehicles available today.

3. Checking Contribution Limits and Eligibility

3.1 IRS Contribution Limits for 2025

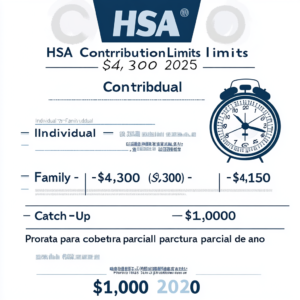

Each year, the IRS sets maximum HSA contributions. In 2025:

Individual Coverage: up to $4,150

Family Coverage: up to $8,300

Catch-Up Contributions (age 55+): additional $1,000

If you’re covered part-year under an HDHP, your limit prorates based on months of eligibility. Exceeding these limits incurs a 6% excise tax until corrected.

3.2 Eligibility Requirements

To contribute in 2025, you must:

Be enrolled in an IRS-defined HDHP

Not be covered by any other non-HDHP health plan

Not be enrolled in Medicare

Not be claimed as a dependent on someone else’s tax return

Staying mindful of eligibility prevents costly mistakes.

4. Strategies to Maximize Your HSA Contributions

4.1 Automating Contributions

I treat my HSA contributions like any other essential bill: automatic and consistent. Setting up payroll deductions through your employer’s benefits portal or scheduling recurring transfers from your checking account ensures you never miss a deposit and smooths out your monthly cash flow. For example, if you earn $60,000 a year and want to hit the individual 2025 limit of $4,150, you can ask HR to deduct roughly $159 per paycheck (26 pay periods). Many banking apps also let you round up everyday purchases and deposit the spare change into your HSA, turning spare cents into serious savings over time. Automating removes decision fatigue, prevents year-end scrambles, and takes advantage of dollar-cost averaging—buying into your HSA throughout the year at different “prices” for any investments you hold.

4.2 Adjusting Mid-Year Contributions

Life changes—raises, new dependents or plan switches—mean your original deduction rate may become outdated. I review my contributions every quarter. If I notice I’m 500 dollars short of the annual limit with two quarters left, I simply increase my per-paycheck amount by $62.50 (500 ÷ 8 pay periods) to catch up. Conversely, if I foresee an over-contribution risk, I reduce or pause deductions temporarily. Use your HSA custodian’s online dashboard to track year-to-date totals and projection tools to forecast whether you’ll hit, exceed or fall short of limits. If your employer’s system is inflexible, make one-time manual transfers to top up or correct your balance. Regular monitoring avoids the 6 percent excise tax on excess deposits.

4.3 Catch-Up Contributions for Savers 55 and Older

Turning 55 unlocks a valuable $1,000 “catch-up” contribution on top of the standard limit. Many of my clients overlook this boost because it must be requested—most payroll systems won’t add it automatically. Contact your benefits administrator before year-end to confirm the extra deduction. If you switch employers mid-year, check whether both plans support catch-ups or if you need to self-initiate contributions through your HSA custodian. Because catch-up funds carry the same triple-tax benefit, maximizing this allowance can significantly enhance your retirement healthcare nest egg with virtually no extra paperwork beyond the initial setup.

5. Integrating Your HSA Into Your Overall Financial Plan

5.1 Budgeting for HSA Contributions

I build HSA funding into my monthly budget as a non-negotiable line item—right alongside rent, utilities and insurance premiums. A simple approach is to allocate a fixed percentage of income (for example, 7 %) to long-term savings, splitting that between retirement accounts and your HSA. If 7 % of your $5 000 monthly take-home is $350, designate $150 to retirement and $200 to your HSA. This ensures you hit IRS limits without feeling stretched. If you prefer a zero-based budget, assign every dollar a job: once you cover essentials, direct surplus cash to your HSA until you meet your goal. For a detailed framework, see our guide “Create a Budget That Works”.

5.2 Coordinating with an Emergency Fund

Your emergency fund and your HSA serve different purposes and should be managed separately. I aim to keep 3–6 months of living expenses in a high-yield savings account for non-medical surprises—job loss, car repairs or urgent home fixes. Meanwhile, my HSA balance grows in a mixture of cash and low-cost investments for healthcare costs. By keeping emergency savings liquid and HSA funds invested, you preserve both your financial safety net and the long-term growth potential of your HSA. If an unexpected medical bill arises and depletes your HSA, you can replenish it before year-end as long as you remain eligible, maintaining your tax-advantaged strategy. For more on emergency planning, check “Plan for Emergencies: Financial Tips”.

6. Investing Your HSA Funds for Long-Term Growth

6.1 HSA Investment Options

Once your balance hits your custodian’s threshold (often $1,000), you can choose among several investment vehicles. Common choices include:

Total-market index funds (e.g. VTI or FSKAX) for broad equity exposure and historically 7–10 % annualized returns

Dividend-paying ETFs (e.g. VIG or SCHD) to generate steady income you can reinvest

Short-term bond funds (e.g. BIV or VGSH) for stability and liquidity

Each option has trade-offs: equities offer higher growth but more volatility, bonds dampen swings but yield less. I typically recommend a 60 % equity / 30 % dividend ETF / 10 % bonds split for younger savers, shifting toward 40/40/20 by age 50. For step-by-step fund selection, see our guide “Secrets of Smart Investing for Beginners”.

6.2 Crafting a Growth-Oriented Strategy

Your HSA can function as a third retirement pillar alongside your 401(k) and IRA. To maximize compounding:

Front-load contributions in January if cash flow allows, capturing more growth time.

Reinvest dividends automatically and set up auto-rebalance at least annually.

Adjust your allocation every 5 years or following major market shifts—many HSA platforms (e.g., Lively, HSA Bank) offer free rebalancing tools.

Harvest tax benefits by using HSA cash for current medical expenses while letting invested funds grow untouched until retirement.

Example: Contributing $4,150/year at age 30 into a portfolio averaging 7 % returns yields over $46,000 by age 65—tax-free, if you avoid early withdrawals.

7. Common Pitfalls and How to Avoid Them

7.1 Over-Contributing and Penalties

Exceeding IRS limits (6 % excise tax per year on the excess) is surprisingly common. To prevent it:

Monitor year-to-date deposits on your custodian’s portal each quarter.

Use Form 5498-SA after tax season to verify contributions reported to the IRS.

Correct excess by withdrawing the overage plus earnings before your tax-filing deadline.

7.2 Non-Qualified Withdrawals

Using HSA funds for non-medical expenses before age 65 triggers ordinary income tax plus a 20 % penalty. Even after 65, non-qualified distributions incur income tax. To avoid missteps:

Keep receipts for every qualified expense (doctor, prescription, dental, vision).

Maintain a spreadsheet of reimbursements, linking each withdrawal to a receipt date.

7.3 Fees and Custodian Terms

Some HSAs charge maintenance or per-trade fees that erode returns. Compare custodians on:

Monthly fees (free vs $3–$4/month)

Expense ratios on investment options (aim for < 0.25 %)

Minimum balance requirements for investing

Switch custodians if fees outweigh your expected tax savings and investment gains.

9. Conclusion

Optimizing your Health Savings Account contributions turns a basic savings tool into a powerful, tax-efficient vehicle that supports both immediate medical expenses and long-term retirement goals. By automating deposits, calibrating contributions mid-year to stay within IRS limits, and investing in low-cost funds, you harness dollar-cost averaging and compound growth.

Coordinating your HSA alongside a separate emergency fund preserves liquidity for unexpected non-medical costs while allowing invested HSA dollars to flourish over decades. Leveraging apps, calculators, and authoritative resources ensures you never miss a contribution opportunity or industry update.

Ready to take full control of your money? This step-by-step online program walks you through budgeting hacks, debt-crushing strategies, and simple investment fundamentals—so you can build real savings and stress-free financial habits.

Explore the full course here.

10. Frequently Asked Questions (FAQ)

Q1: Can I change my HSA contribution amount mid-year?

As you learn How to Optimize Your HSA contributions, it’s important to know you can adjust your deposit schedule at any time. Most employers allow you to modify payroll deductions through the benefits portal, enabling you to increase or decrease contributions based on life events—raises, new dependents, or plan changes. If your system is inflexible, you can always make a one-time manual transfer via your HSA custodian’s website. I recommend reviewing your year-to-date contributions quarterly and adjusting immediately to stay within IRS limits and avoid the 6% excise tax on excess deposits.

Q2: What medical expenses qualify for HSA withdrawals?

Mastering How to Optimize Your HSA contributions means using funds only for IRS-approved costs. Qualified expenses include doctor and specialist visits, prescription medications, dental treatments (fillings, root canals, braces), vision care (eye exams, glasses, contacts), and certain over-the-counter items with a prescription. The IRS Publication 502 offers a comprehensive list—from acupuncture to durable medical equipment. To maintain your tax-free status, keep detailed receipts and organize them by date and expense type, either in a physical folder or uploaded to your custodian’s digital portal.

Q3: How do HSA contributions affect my tax return?

Understanding How to Optimize Your HSA contributions is incomplete without grasping their tax impact. Each dollar you deposit lowers your taxable income on Form 1040 via Schedule 1 and Form 8889, potentially saving you hundreds in federal and state taxes. Employer contributions show up in Box 12 of your W-2 with code W, automatically reducing your reported wages. After filing, verify Form 5498-SA matches your records to ensure accurate IRS reporting. Any investment gains remain tax-free as long as withdrawals align with qualified medical expenses.

Q4: What happens if I switch jobs or health plans?

A key principle of How to Optimize Your HSA contributions is portability. Your HSA balance stays with you—even if you change employers or plans. If you move to a non–high-deductible plan or enroll in Medicare, you can no longer contribute but can still spend existing funds tax-free on qualified expenses. When changing custodians, consider rolling balances over to consolidate investments, reduce fees, and simplify management. Most custodians facilitate trustee-to-trustee transfers with minimal paperwork.

Q5: Can I use HSA funds for my family members?

To fully embrace How to Optimize Your HSA contributions, remember you may reimburse qualified medical costs for your spouse and IRS-defined dependents, even if they aren’t covered under your HDHP. Examples include a child’s orthodontic work or a spouse’s mental health counseling. Each expense must occur after HSA establishment and be documented with receipts. This household approach extends your triple-tax advantage across your entire family, amplifying the impact of every contribution you make.

Q6: What investment strategies work best inside an HSA?

An essential step in How to Optimize Your HSA contributions is choosing the right investment mix. Keep one to two years’ worth of expected medical expenses in cash for liquidity, then allocate remaining funds into diversified, low-cost index funds or dividend ETFs. Younger savers can target an 80/20 equity-to-bond split, gradually shifting toward a more conservative 50/50 or 40/60 mix after age 50. Automate dividend reinvestment and rebalance annually to maintain your target allocation, leveraging your custodian’s free rebalancing tools where available.

Q7: How do catch-up contributions work for savers over 55?

As part of How to Optimize Your HSA contributions, savers aged 55 and older can add a $1,000 catch-up deposit above the standard annual limit. Unlike regular contributions, catch-ups aren’t auto-enrolled—request this increase through your HR or benefits portal before year-end. If you change employers mid-year, confirm both plans support catch-ups or self-initiate the extra deposit via your custodian’s website. This additional allowance, with the same triple-tax benefit, can significantly boost your retirement healthcare savings.

Q8: Are there fees I should watch out for?

Fee management is critical when How to Optimize Your HSA contributions. Compare custodians on maintenance fees (ideally $0–$3/month), investment expense ratios (aim below 0.25%), and transaction or trading charges. Watch for minimum balance requirements to avoid inactivity fees or unlocking investment privileges. If fees outweigh your expected tax savings and growth potential, consider migrating to a low-fee provider like Lively or Fidelity HSA, which offer free investing and no maintenance costs.

Q9: What records do I need for IRS compliance?

Organizing documentation is vital to How to Optimize Your HSA contributions with confidence. Retain all custodian statements showing contributions and distributions, itemized receipts for qualified expenses, Form 5498-SA (contributions report), and Form 1099-SA (distributions report). Keep your W-2 (Box 12, code W) for employer deposits. Store these records—digital or physical—in a single, secure folder. Well-maintained files simplify tax filing and protect you during an IRS audit.

Q10: Can I use HSA funds for non-medical expenses in retirement?

One advanced tactic in How to Optimize Your HSA contributions is leveraging post-retirement flexibility. After age 65, you can withdraw funds for non-qualified expenses without penalty—though distributions become subject to ordinary income tax, akin to a traditional IRA. To maximize benefits, continue using HSA withdrawals for healthcare costs tax-free and treat any surplus as a supplemental retirement fund. This dual-purpose capability makes HSAs uniquely versatile compared to other savings vehicles.

{kind=link}